Lending teams in 2026 are caught between two pressures that pull in opposite directions. Per-loan costs continue to increase; defect rates, after a slight decrease from previous years, have increased again, and the borrowers now expect same-day lending decision rather than an older style underwriting process.

At the same time, most equipment leasing companies, CDFIs, and mid-sized banks still rely heavily on using Excel spreadsheets, e-mail chains, and re-keying borrower information as part of their pipeline management.

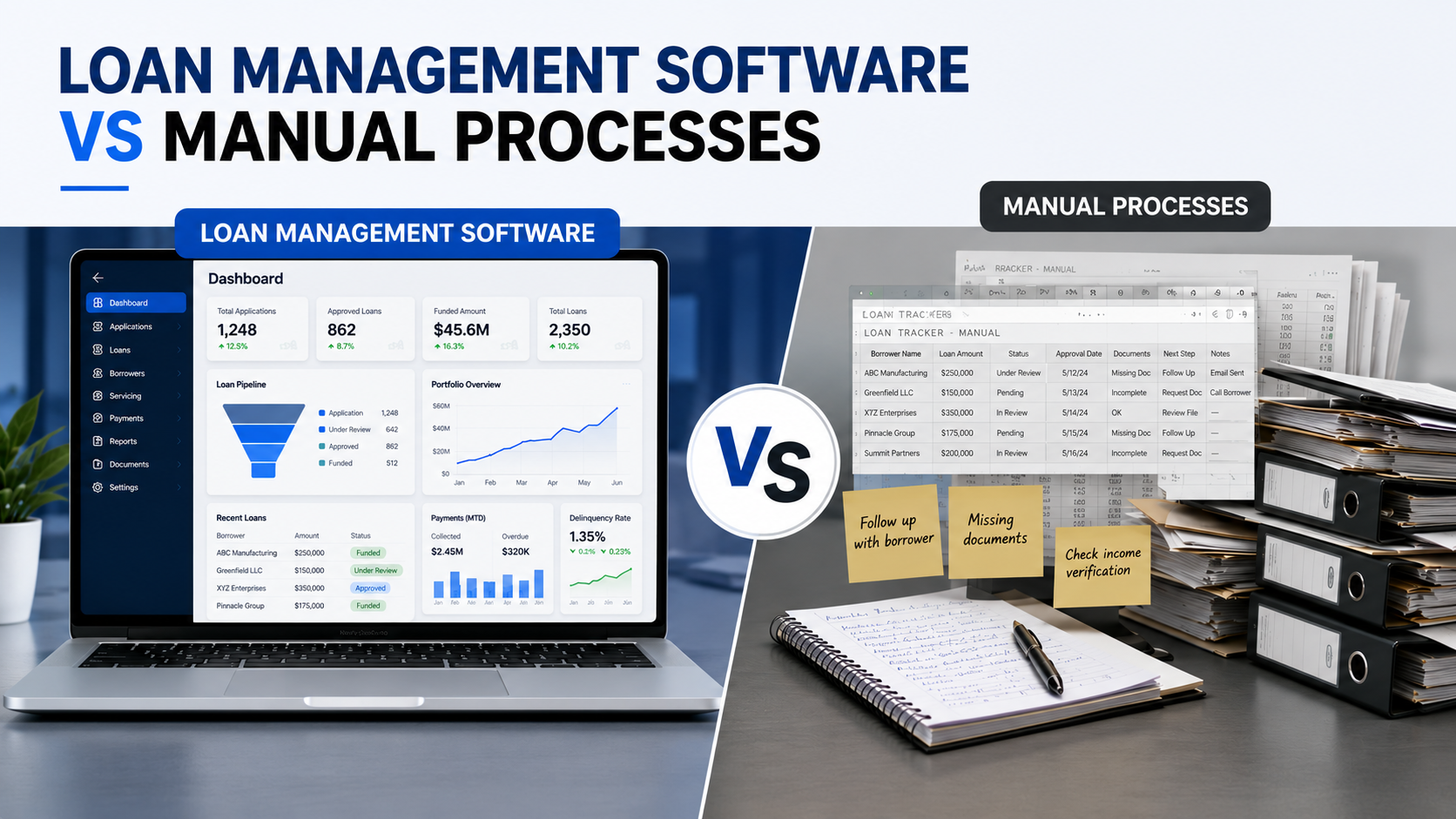

A modern loan management software changes that equation, and the gap between automated lenders and manual ones is widening every quarter. This breakdown walks through the differences in terms of speed, cost, accuracy, regulatory compliance, and scalability.

Loan Management Software Replaces Manual Processes By Automating The Lending Lifecycle And Improving Efficiency

A Loan Management Software is a unified digital platform that manages all aspects of lending lifecycle including application intake, underwriting, document collection, funding, servicing, collections and reporting.

Manual processes break this same loan lifecycle into disparate pieces, with borrower data entered manually across tools, payments tracked on spreadsheets, and compliance checks performed by analysts working from inconsistent templates.

That point has passed as a requirement. As loan volume continues to increase so too will the need for Lenders to adopt Loan Origination Systems (LOS). The global loan origination software market is expected to continue its rapid growth from $6.58 Billion in 2025 to $10.3 Billion by 2029 at a 12.1% CAGR, with adoption now extending well beyond large banks to credit unions, community lenders, and specialty finance firms.

With increased volume, borrowers' expectations, and regulatory requirements, traditional manual processes just can’t keep up.!

Loan Management Software Reduces Cycle Times by Eliminating Manual Process Delays

Manual loan processing is time consuming, often taking several weeks. Each of the loan steps (intake, verification, underwriting, funding) requires a person to manually move it along. The same data has to be re-keyed at every step of the way, documents have to be chased down via e-mail, and the exceptions hang out in the inbox waiting for someone to act on them.

The entire process can be streamlined by automation. It removes the hand-offs from one person to another by validating the data upon entry, obtaining credit reports and bank statements through API calls, and providing configurable workflows for the files.

For lenders who want to evaluate a loan origination software based on speed and efficiency, features like audit ready intake, automated underwriting, and customizable approval logic cut approval cycles from weeks to days, while improving review quality.

Manual Workflows Increase Cost Per Loan Through Hidden Operational Inefficiencies

Manual processing can have a huge negative impact on profitability through labor, occupancy, and compensation for repetitive tasks, and all these costs are directly related to volume. As the number of applications increases, so does the increase in overhead costs.

As stated by the Mortgage Bankers Association, the production cost of loans rose to $12,579 in the first quarter of 2025 from $11,230 in the previous quarter. Personnel costs were the greatest share of those costs.

A Loan Management Software reduces this cost base in three ways:

- It eliminates duplicate data entry into origination, servicing and reporting systems.

- It automates document collection, fee calculation and compliance reviews, reducing analysts’ hours doing these activities.

- It provides a way for lenders to grow their application volume while maintaining their staff levels.

For CDFIs, Fintechs and community banks watching every basis point of profit margin, these operational efficiencies often pay back the platform investment within one fiscal year.

Automated Loan Management Software Improves Accuracy and Reduces Loan Defects

Manual processes are prone to making errors at every keystroke. Income figures are entered incorrectly, employment information may be recorded differently on forms and therefore may never match for underwriting purposes. These mistakes compound to repurchase risk and buyback exposure.

As per the ACES’ Mortgage QC Industry Trends Report, the critical defect rate rose to 1.31%, ending a two-quarter streak of improvement, with income/employment reclaiming its spot as the leading category of defects.

NOTE: A critical defect is defined as a defect that would result in the loan being uninsurable or ineligible for sale.

Loan management systems address the same failures by retrieving all borrower information at once from source documents, validating this information against other sources, and ensuring accuracy prior to submission to an underwriter.

Besides, audit trails provide documentation for each entry, approval, or updated condition, which is exactly what regulatory bodies and investors want to find when reviewing a file.

Loan Servicing Software Beats Spreadsheets on Audit Day

Once loans are booked, manual servicing presents its own set of issues. Borrowers' escrow accounts, delinquencies, covenants, and communications become disorganized in separate systems. Lenders can identify potential risk factors during quarterly reviews but the actual occurrence can be missed.

Automating loan servicing allows lenders to track their portfolios in real time, configure custom monitoring criteria, and automate alerts if a borrower violates a covenant, misses a payment, or changes to a higher risk category. The use of standard templates ensures that all borrowers are reviewed using the same logic, which is the key to maintaining accurate servicing records.

The quality impact of these tools is measurable. According to Freddie Mac's 2025 Cost to Originate Study, those lenders who use automated underwriting features extensively report approximately 40% less defective loans as compared to those with low automation usage.

Fewer defective loans signify reduced demand for repurchases by investors, decreased compliance penalties from regulatory bodies, and improved long-term performance of portfolios.

End-to-End Loan Management Software Enables Scalable Portfolio Growth and Future-Proofs Lenders

Manual lending activities hit a "ceiling" which is the number of files that an analyst can work on per day. When volume exceeds this threshold, lenders are forced to either add staff at a rapid pace or experience longer turn times and lower quality. Neither option is long-term viable for lenders operating in a market where origination margin are already compressed.

Cloud Maven, Inc’s cmLending is a Salesforce-native loan management system that integrates origination, servicing, syndication and lease management.

- Workflows are customized to fit each lender's product instead of forcing "one size fits all” process

- The platform integrates with over 175 third-party APIs to handle verification and payment information

- Reports are pulled from a single source of truth instead of reconciled exports.

Why Loan Management Software Wins Against Manual Processes in 2026

The argument for eliminating manual processes has moved from theory to reality. Production costs per loan have risen significantly beyond long term averages. Defect rates continue to rise as do borrower decisions to go with whatever lender makes a decision the fastest.

A unified Loan Management Software provides an operational solution to this pressure by replacing re-keying, emailing, and spreadsheets with one connected lending platform.

Built for lenders who wish to consolidate origination, servicing, syndication, and lease management into one Salesforce-based system, cmLending platform is designed for this exact transition.

Book a demo to view how the platform removes the manual levels you still work through.