Commercial lending is becoming bigger, faster, and more complicated. Borrowers are pursuing bigger acquisitions, infrastructure projects require larger amounts of money, and lenders face tighter concentration limits while trying to protect their margins.

That shift is clearly visible in the syndicated lending market. According to the Bank for International Settlements, the global syndicated loan volume increased by approximately 35% to almost $6 trillion in 2025 due to large corporate refinancings and increased demand for AI infrastructure financing.

However, lenders are under pressure to process deals quicker while controlling risk exposure, regulatory compliance obligations, and investor reporting.

This is why Loan Syndication becomes important for banks, private lenders, credit unions, and commercial finance institutions that want to fund larger deals without taking on disproportionate risk.

While loan syndication can be a vehicle for expanding your business's loan originations, managing multiple lenders, structuring payments, communicating with borrowers, and servicing workflows can create operational complexity.

Here are some things lenders should understand about loan syndications, how they function, and when it may make financial sense to utilize loan syndications.

What Is Loan Syndication?

Loan syndication is a type of lending arrangement where multiple financial institutions share the responsibility to fund a single borrower via one structured loan agreement. Instead of one lender taking on the full exposure of a large commercial loan, the loan is divided among multiple participants.

A lead lender (or "arranger") typically originates the transaction and determines whether the loan exceeds its internal lending guidelines or creates unnecessary concentration risks. The lead lender then invites other financial institutions to share in funding a portion of the loan.

Loan syndication is most commonly used in commercial real estate, infrastructure development, leveraged buyouts, mergers/acquisitions, healthcare expansion projects, and large equipment financing.

For instance, if a borrower needs a $400 million loan for an acquisition and a regional bank can only lend $100 million, the bank may utilize syndication. By doing so, the bank retains the customer relationship and distributes the remainder of the loan amount ($300 million) to participating lenders.

To borrowers, loan syndication allows access to large funds. To lenders, syndicated lending creates growth opportunities without requiring excessive balance sheet exposure.

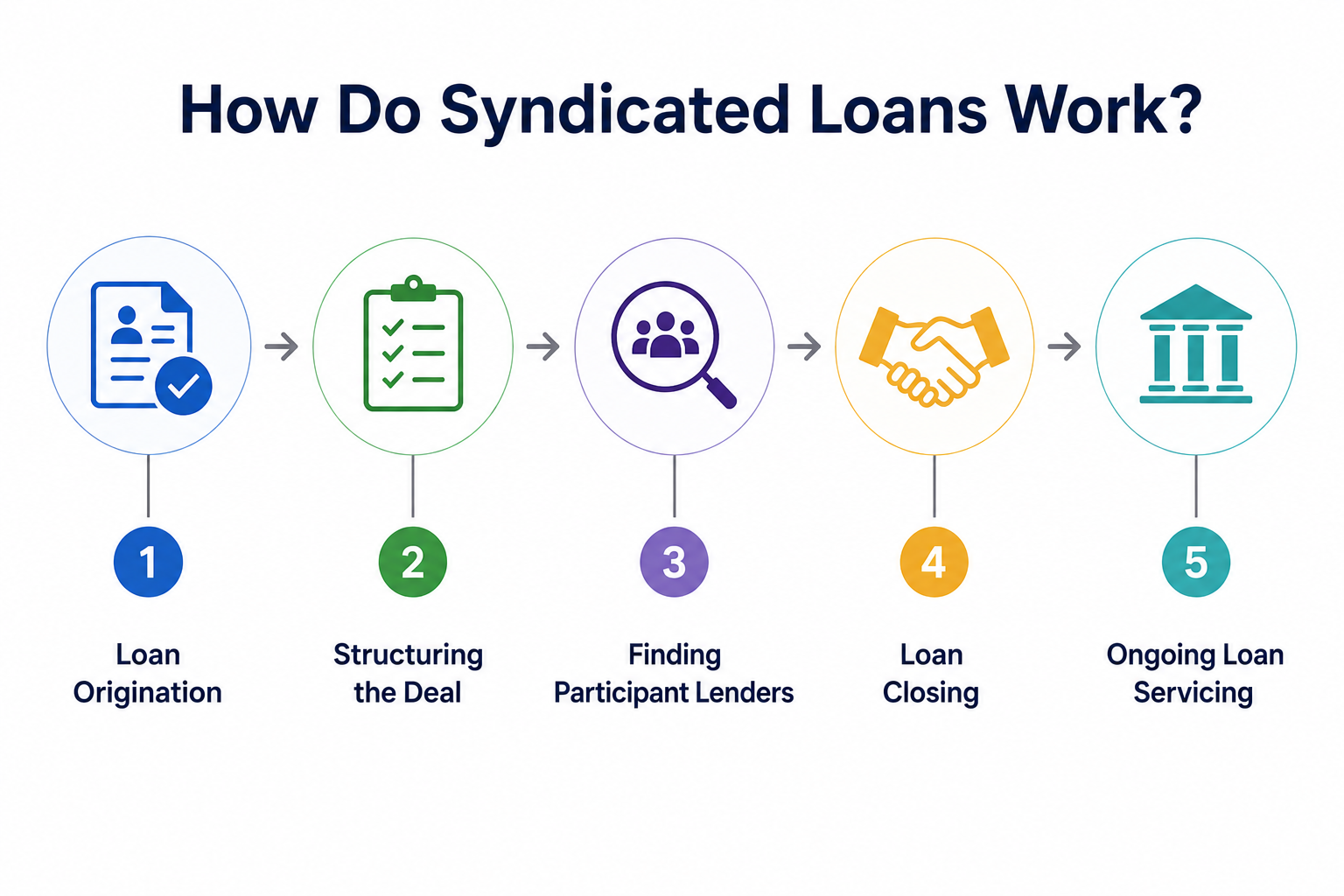

How Do Syndicated Loans Work?

The syndicated loan process begins when an applicant seeks funds from a single lender. The amount requested can be greater than what one lender would willingly or be capable of funding independently.

Loan Origination

A lead lender first reviews the applicant's financial record, collateral position, repayment capacity, and transaction reason. If there is potential for a profitable opportunity consistent with their lending goals but exceeding their maximum acceptable risk level, the lender structures the deal for syndication.

Structuring the Deal

The lead lender defines key terms regarding the loan including interest rate, payment schedule, covenants requirements, collateral structures, and ownership percentage that each lender holds.

Finding Participant Lenders

The lead lender markets portions of the loan to participating lenders. These consist of commercial banks, institutional investors, regional lenders, private debt companies, or credit unions.

Loan Closing

Once commitments are secured, the next step is closing. At this stage, funds are disbursed, contracts are executed, and servicing responsibilities are assigned.

Ongoing Loan Servicing

To ensure timely payments to all participating lenders, covenant tracking, borrower communications, investor reports and compliance obligations are managed across all participants.

Loan Syndication Relies on Multiple Participating Parties

For syndicated lending to occur effectively, coordination is necessary among stakeholders.

The Lead Arranger originates the loan, develops the structure for the transaction, and identifies participating lenders. As a rule, the lead arranger maintains the largest stake in the borrower relationship.

The Agent Bank manages the post-closing administrative tasks related to the syndicated loan. Such tasks include receiving payment from borrowers, dispersing proceeds to lenders, preparing/issuing notifications, maintaining documentation, etc.

Each Participating Lender contributes capital to the loan and receives income based upon its share of the loan.

Borrower engages primarily with the lead arranger but remains accountable to all terms contained within the syndicated loan agreement.

Besides, compliance teams, legal teams and loan servicing teams ensure that all documents are properly completed and compliant with applicable regulations.

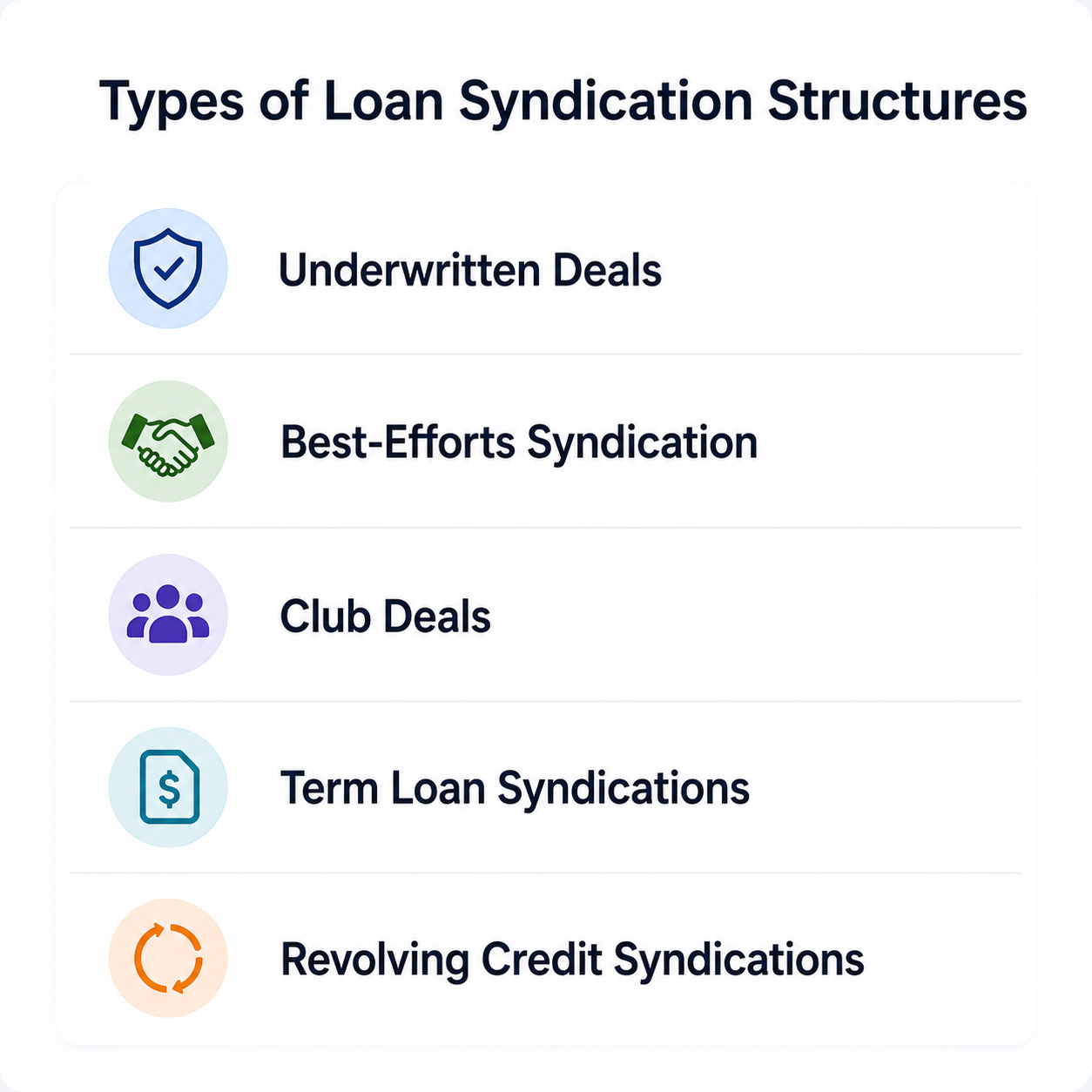

Types of Loan Syndication Structures

Not all syndicated loans are structured the same way.

Underwritten deals

The lead lender has "skin in the game" regardless of whether or not they are able to attract other investors. This provides certainty for the borrower but creates risk for the lead lender.

Best-efforts syndication

The arranger tries to find participants for the deal, but there is no guarantee that the deal gets fully funded. This reduces the risk for the arranger.

Club deals

These types of deals consist of a small number of investors who collectively lend money to the borrower. They are most commonly used for middle-market transactions.

Term loan syndications

This provides the borrower with a lump sum payment schedule.

Revolving credit syndications

This type allows the borrower to take out cash as needed from the total available line of credit.

As demand for debt continues to rise so do new ways of structuring these deals. Last year, as reported by BMO Capital Markets, the U.S. leveraged loan issuance reached $550 billion to $600 billion in 2025, representing a 77% YoY increase.

This increased volume is creating additional opportunities for lenders to participate in larger syndicated loan agreements.

Why Lenders Use Loan Syndication

Risk distribution is probably the largest advantage of using loan syndication.

Rather than placing large capital behind one client or one project, lenders distribute the exposure among multiple institutions.

This is especially helpful when financing large commercial real estate projects, making a large acquisition or developing infrastructure as each of those activities creates concentration risks.

Another reason that many lenders use loan syndication is because it gives them the opportunity to service larger clients which may be lost to national banks and private credit firms.

Lead arrangers can also earn additional income through origination fees, servicing fees and administrative fees, and maintain a relationship with the borrower.

Diversifying one's portfolio is yet another key advantage of loan syndication. Instead of investing a lot of capital into one transaction, lenders can invest in several transactions across various industry sectors.

This flexibility gives lenders a better chance at growing their loan portfolios in a strategic manner.

When Should Lenders Use Loan Syndication?

Loan syndication becomes particularly valuable when borrowers require capital that exceeds a lender’s internal exposure limits.

This often happens during mergers & acquisitions, infrastructure financing, healthcare expansions, and large commercial development projects.

The trend is accelerating globally. According to the OECD Global Debt Report, outstanding syndicated loans totaled $25.4 trillion by the end of 2024, indicating further demand from borrowers for large scale financing.

Besides, when lenders enter an unknown industry or geographic region, syndicated lending is often an attractive option to share some level of risk with a partner that is well-established in that area.

Finally, economic volatility is likely to make lenders want to share the risk instead of concentrated lending positions.

Challenges of Managing Syndicated Loans

Although syndicated lending has opened up new avenues for growth, it also has brought about new operational challenges.

Most lenders have historically relied on manual methods such as email, spreadsheets and/or disconnected systems to manage onboarding, investor participation, borrower communication, and payment allocation.

Manual processes create delays, errors in reports, and an increased amount of regulatory risk.

As loan volume grows so do the inefficiencies associated with loan syndications.

How Technology Simplifies Loan Syndication

Modern lenders need infrastructure built specifically for syndicated lending.

Cloud Maven, Inc Loan Syndication solution helps lenders automate participation management, investor tracking, payment waterfall, reporting workflow, and compliance documentation.

Unlike other solutions that require lenders to use and maintain separate systems to manage syndication related activities, they now consolidate their syndication-related activities using a single system.

When paired with cmLending platform, lenders may leverage a connected ecosystem to manage all aspects of loan origination, loan servicing, and loan syndication.

That creates faster execution, fewer operational errors, and better scalability.

Loan Syndication vs Private Credit vs Direct Lending

Syndication is a much better way of funding big deals with lots of money and managing your risk diversified than private credit or direct lending.

Direct lending puts all the risk on one person/lender.

Big deals, where you need lots of money to make them happen but don't want to be putting it all on your own shoulders is what loan syndication was made for.

Lenders who want to do bigger deals but not put too much capital at risk, for them syndicated lending continues to be a good option.

Cloud Maven, Inc Helps Lenders Scale Syndicated Lending Operations

Loans Syndication allows lenders to create more financing options for bigger deals, reduces their exposure risk, and competes in an ever increasing complex credit market.

But growth alone is not enough. Without strong operational infrastructure, syndicated lending can become difficult to scale.

Manually tracking different lenders using just spreadsheets or separate systems causes slowdowns in execution and increases the risk associated with servicing.

For lenders looking to scale syndicated lending operations, Cloud Maven, Inc’s Loan Syndication and cmLending provide the infrastructure needed to manage syndicated loans efficiently from origination through servicing.